When someone donates to a nonprofit organization, it may feel simple — make a contribution, receive a receipt, and claim a tax deduction. But things become more complex when the donor receives goods or services in return.

Did someone pay to attend a fundraising gala and receive dinner?

Did a donor contribute and receive merchandise?

Did a sponsor receive advertising or promotional benefits?

In these situations, the IRS has strict rules governing how receipts must be issued and how deductions are calculated. Understanding these requirements is essential for both nonprofits and donors to remain compliant with U.S. tax law.

This guide explains everything clearly, using practical examples and plain language.

What “Benefits Received” Means

“Benefits received” refers to goods or services a donor receives in exchange for a contribution.

If a donor receives something of value, the IRS does not allow a deduction for the full donation amount. Only the portion that exceeds the value of what was received may qualify as a charitable deduction.

This type of contribution is known as a quid pro quo donation.

Understanding Quid Pro Quo Donation Rules

A quid pro quo contribution occurs when a donor makes a payment that is partly a charitable gift and partly a payment for goods or services.

For example, if a donor gives $200 to attend a charity event and the dinner provided has a fair market value of $60, only $140 may be tax-deductible.

The IRS requires nonprofits to clearly disclose the value of the goods or services provided and inform the donor that only the excess amount is deductible.

If the organization fails to provide this written disclosure when required, penalties may apply.

How to Calculate the Tax-Deductible Portion

The calculation is straightforward.

The deductible amount equals the total contribution minus the fair market value (FMV) of the goods or services received.

For example, if someone donates $500 to attend a charity golf tournament and the value of the tournament package is $150, then $350 is potentially deductible.

If a donor pays an amount equal to or less than the FMV of what they receive, there is no deductible contribution.

Fair Market Value (FMV) Requirements

Fair market value means the price an item or service would sell for on the open market.

Nonprofits must make a good-faith estimate of the FMV of goods or services provided in exchange for donations. This estimate should reflect realistic market pricing. It should not be inflated or artificially reduced to increase the donor’s deductible amount.

Organizations can determine FMV by reviewing comparable retail prices, vendor invoices, or similar event pricing.

Accurate valuation is important because incorrect reporting may create issues during an IRS audit.

IRS Written Disclosure Rule for Contributions Over $75

If a donor makes a quid pro quo contribution exceeding $75, the nonprofit must provide a written disclosure statement.

This statement must:

- Inform the donor that the deductible amount is limited to the excess over the value of goods or services received

- Provide a good-faith estimate of the value of those goods or services

Failure to provide this disclosure can result in a penalty of $10 per contribution, up to $5,000 per fundraising event.

This requirement applies even if the deductible portion is small.

The IRS $250 Substantiation Rule

Separate from the $75 disclosure rule is the $250 substantiation requirement.

If a donor makes a single contribution of $250 or more, the donor must obtain a written acknowledgment from the charity before claiming a deduction.

The acknowledgment must include:

- The organization’s name

- The amount of cash contributed or a description of non-cash property

- A statement indicating whether goods or services were provided

- A description and good-faith estimate of their value, if applicable

A bank record alone is not sufficient for donations of $250 or more.

What Information Must Appear on a Compliant Donation Receipt

A compliant receipt should clearly include the organization’s legal name, the date of the contribution, and the total amount donated.

It must also include a clear statement indicating whether goods or services were provided in exchange for the donation. If they were provided, the receipt must include a good-faith estimate of their fair market value.

If no goods or services were provided, the receipt must clearly state that fact.

If only intangible religious benefits were provided, the receipt must state that instead.

Clarity and transparency are essential.

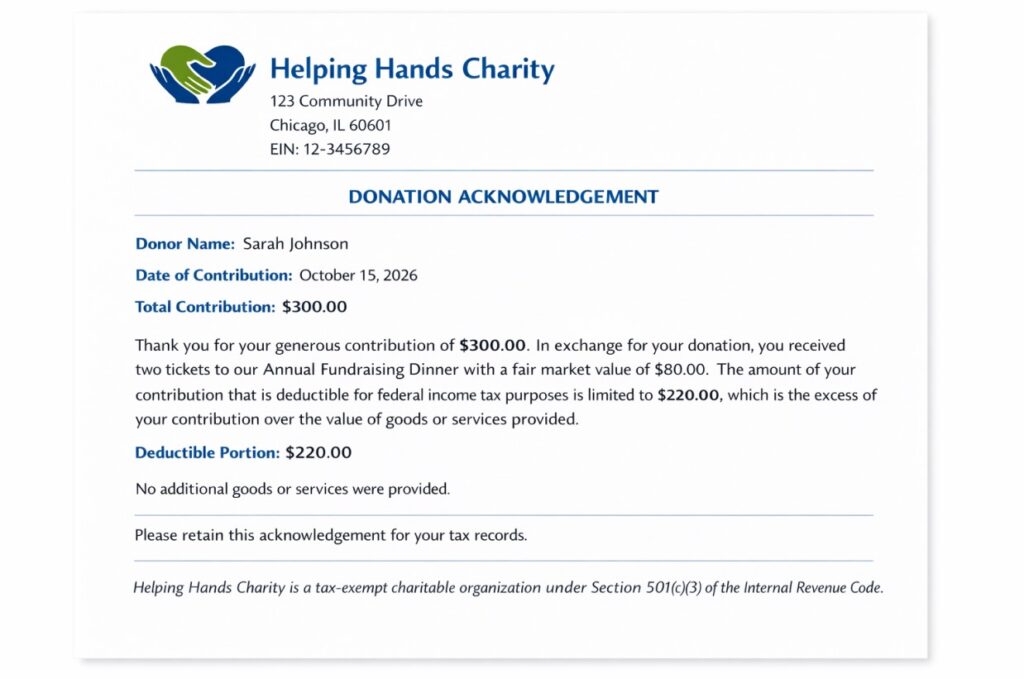

Example of an IRS-Compliant Donation Receipt

Below is an example of how a proper receipt might look when a donor receives goods or services in return:

Helping Hands Charity

123 Community Drive

Chicago, IL 60601

EIN: 12-3456789

Donation Acknowledgment

Donor Name: Sarah Johnson

Date of Contribution: October 15, 2026

Total Contribution: $300.00

Thank you for your generous contribution of $300.00. In exchange for your donation, you received two tickets to our Annual Fundraising Dinner with a fair market value of $80.00. The amount of your contribution that is deductible for federal income tax purposes is limited to $220.00, which is the excess of your contribution over the value of goods or services provided.

No additional goods or services were provided.

Please retain this acknowledgment for your tax records.

This example demonstrates transparency. It clearly states the total contribution, the value of benefits provided, and the deductible portion.

If no goods or services had been provided, the receipt would instead state: “No goods or services were provided in exchange for this contribution.”

Sample Donation Receipt Image for Reference

(This is a dummy receipt shown for illustration purposes only. All names and details are fictitious.)

When Donations Are Not Deductible

Certain payments are not tax-deductible, even if made to a nonprofit organization.

Raffle tickets are never deductible. If someone purchases a raffle ticket, the entire amount is considered payment for the chance to win.

Membership fees may not be deductible if they provide significant benefits.

Payments made to individuals are not deductible.

Political contributions are not deductible.

Payments that equal the fair market value of goods or services received are not deductible.

Donors should also confirm that the organization is recognized as a qualified 501(c)(3) public charity.

Exceptions for Token or Insubstantial Benefits

The IRS allows limited exceptions when the value of goods or services provided is minimal.

If a nonprofit provides a small promotional item, such as a low-cost pen or calendar bearing the organization’s name, the benefit may be considered insubstantial. In those cases, the full donation may still be deductible.

Similarly, certain annual memberships costing $75 or less may qualify for full deductibility if benefits are limited to things such as newsletters, free admissions, or small discounts.

The IRS updates dollar thresholds periodically, so organizations should review current guidance each year.

Why IRS-Compliant Receipts Matter

IRS-compliant receipts protect both nonprofits and donors. For nonprofits, accurate documentation reduces the risk of penalties and strengthens internal controls. It demonstrates professionalism and accountability.

For donors, proper receipts are essential for claiming deductions and responding to any IRS inquiry. Without a compliant acknowledgment, a donor may lose the ability to deduct a contribution.

Beyond legal requirements, clear receipts build trust. When donors see transparency in how contributions are handled, confidence in the organization grows.

Compliance is not simply a regulatory obligation; it is a foundation for credibility.

Making IRS-Compliant Receipts Easier with Automation Tools

Even when nonprofits understand IRS rules, the hard part is often execution: calculating fair market value, applying quid pro quo language, ensuring the $250 acknowledgment elements are present, and sending receipts on time. Manual processes can lead to common issues like missing required statements, inconsistent wording, or incorrect deductible amounts—especially when events, sponsorships, or auctions are involved.

This is where donation receipt automation tools can help. Tools like Donorkite are designed to streamline compliant acknowledgments by standardizing receipt language, capturing key fields, and producing consistent documentation for donors. For nonprofits with frequent contributions, event tickets, or benefit-based donations, automation can reduce human error and make recordkeeping easier during audits or donor questions.

The key is not the tool itself, but the outcome: receipts that are accurate, timely, and aligned with IRS requirements—particularly for quid pro quo contributions and gifts of $250 or more.

Final Thoughts

IRS rules about benefits received are designed to make sure donors only deduct the true charitable portion of their contributions. When goods or services are provided, only the amount above their fair market value is tax-deductible. Nonprofits must give proper written disclosures for quid pro quo donations over $75 and written acknowledgments for single contributions of $250 or more. Clear wording, accurate fair market value estimates, and complete documentation are essential for compliance.

By following these requirements carefully, nonprofits can reduce audit risk and protect their organization’s credibility. Donors, in turn, can confidently claim their deductions knowing they have the proper documentation. Staying compliant is not just about meeting IRS standards—it’s about maintaining transparency, trust, and good financial stewardship.