Issuing donation receipts is not merely an administrative task. In Sri Lanka, it is a statutory responsibility. Registered charities, trusts, and approved nonprofit organizations must comply with Inland Revenue Department (IRD) regulations when issuing receipts—especially when donations are intended to be tax-deductible.

Non-compliance can result in denied tax claims for donors, financial penalties, audit scrutiny, and reputational damage. For nonprofit leaders, accountants, and compliance officers, understanding IRD-compliant donation receipt requirements in Sri Lanka is essential for maintaining regulatory integrity and donor confidence.

Legal Framework Governing Donation Receipts in Sri Lanka

Donation receipting is primarily governed by:

- Inland Revenue Act No. 24 of 2017

- IRD regulations and administrative guidelines

- Conditions attached to approved charitable institution status

Only organizations formally approved by the Inland Revenue Department are permitted to issue tax-deductible donation receipts. Approval confirms that the entity meets the legal definition of a charitable institution under Sri Lankan tax law.

Without IRD approval, an organization may acknowledge donations, but donors will not qualify for tax deductions.

Eligibility to Issue Tax-Deductible Donation Receipts

The following entities may issue IRD-recognized donation receipts:

- Registered charities approved under the Inland Revenue Act – These organizations must be formally recognized by the Inland Revenue Department as approved charitable institutions. Approval confirms that donations made to them may qualify for tax deductions, subject to legal limits and conditions.

- Charitable trusts with valid IRD approval – Trusts established for charitable purposes must obtain specific IRD authorization before issuing tax-deductible receipts. The trust deed and activities must align with approved charitable objectives.

- Nonprofit organizations granted approved charitable status – NGOs and nonprofit entities that meet regulatory requirements and receive IRD approval can legally issue compliant donation receipts for tax purposes.

Maintaining approved status is critical. If recognition is suspended or revoked, the organization cannot legally issue tax-deductible receipts during that period.

Mandatory Requirements for an IRD-Compliant Donation Receipt

An IRD-compliant donation receipt must contain specific information to ensure validity, traceability, and tax compliance.

Organizational Details

The receipt must clearly state:

- Full legal name of the organization (exactly as registered)

- Registered address

- Charity registration number

- IRD approval or reference number (where applicable)

Accuracy in these details is essential, as discrepancies can invalidate donor tax claims.

Receipt Identification Details

Each receipt must include:

- A unique, sequential receipt number

- Date the donation was received (not merely the issue date)

Sequential numbering is particularly important for audit trails and financial reconciliation.

Donor Information

The following donor details should be recorded:

- Full name of the donor (individual or corporate)

- Donor address (strongly recommended for audit support)

Correct donor identification supports both compliance and tax reporting.

Donation Information

The receipt must specify:

- Exact amount received in Sri Lankan Rupees

- Amount written in both numbers and words (best practice)

- Mode of payment (cash, cheque, bank transfer, online payment)

- Transaction reference or cheque number where applicable

The receipt must also include a statement confirming that the payment is a voluntary donation and that no goods or services were provided in exchange.

Authorization

The receipt should contain:

- Signature of an authorized officer

- Name and designation of the signatory

- Official seal or stamp of the organization

These elements confirm authenticity and internal authorization.

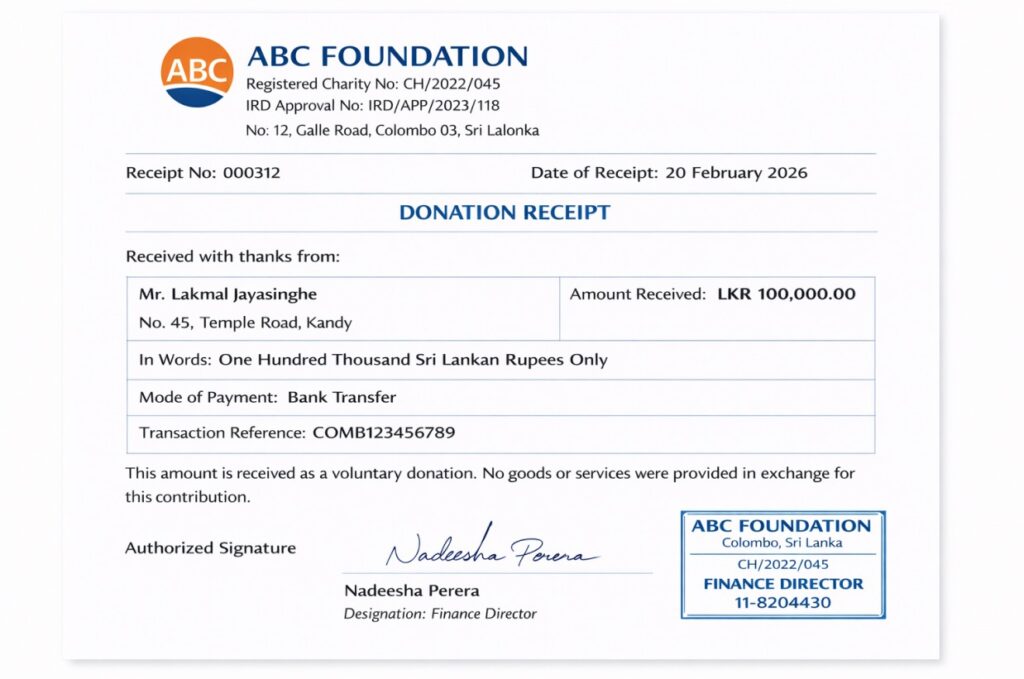

Example of an IRD-Compliant Donation Receipt Format

Below is a professional sample format:

ABC Foundation

Registered Charity No: CH/2022/045

IRD Approval No: IRD/APP/2023/118

No. 12, Galle Road, Colombo 03, Sri Lanka

Receipt No: 000312

Date of Receipt: 20 February 2026

Received with thanks from:

Mr. Lakmal Jayasinghe

No. 45, Temple Road, Kandy

Amount Received: LKR 100,000.00

In Words: One Hundred Thousand Sri Lankan Rupees Only

Mode of Payment: Bank Transfer

Transaction Reference: COMB123456789

This amount is received as a voluntary donation. No goods or services were provided in exchange for this contribution.

Authorized Signature

Name: Nadeesha Perera

Designation: Finance Director

Official Stamp

This format includes all mandatory compliance elements required under IRD standards.

Sample Donation Receipt Image for Reference

(This is a dummy receipt shown for illustration purposes only. All names and details are fictitious.)

Tax Compliance and Donor Deduction Rules

Under the Inland Revenue Act, donations made to approved charitable institutions may qualify for tax deductions, subject to prescribed limits and conditions.

For a donor to claim a deduction:

- The organization must hold valid IRD approval

- The donation must meet qualifying conditions

- The receipt must contain all required information

If a receipt lacks mandatory details, the Inland Revenue Department may reject the deduction claim. Therefore, compliance protects both the donor and the organization.

Record-Keeping and Documentation Standards

Issuing a compliant receipt is only part of the obligation. Registered charities must maintain comprehensive and accurate records.

Required Record-Keeping Practices

Charities should:

- Retain copies of all issued receipts (physical or digital)

- Maintain a structured donor register

- Reconcile receipt numbers with accounting records

- Match donations with bank statements

- Retain records for a minimum of six to seven years

Proper documentation ensures readiness in case of IRD audits or regulatory reviews.

Penalties for Non-Compliance

Failure to comply with IRD donation receipt requirements can lead to significant consequences.

Possible actions by the Inland Revenue Department include:

- Disallowing donor tax deductions

- Imposing financial penalties

- Conducting detailed tax audits

- Revoking approved charitable status

Loss of IRD approval can severely impact fundraising capacity and organizational credibility.

Common Compliance Mistakes

Even established charities may encounter compliance issues due to administrative oversight. Common mistakes include:

1. Issuing receipts without sequential numbering

Sequential numbering creates a clear audit trail. When receipts are not issued in proper order, it becomes difficult to track missing or duplicate receipts. During an IRD audit, gaps in numbering may raise concerns about internal controls and financial transparency.

2. Omitting IRD approval numbers

The IRD approval number confirms that the organization is authorized to issue tax-deductible receipts. If this number is missing, donors may face difficulties when claiming tax deductions. It can also signal non-compliance during regulatory reviews.

3. Incomplete donor details

Missing or incorrect donor names and addresses can weaken the validity of a receipt. Accurate donor identification is important for tax purposes and audit verification. Incomplete information may result in rejected tax claims or compliance queries.

4. Failing to record payment method

The receipt should clearly state whether the donation was made by cash, cheque, bank transfer, or online payment. Without this information, reconciling financial records becomes difficult. Clear payment records support transparency and financial accuracy.

5. Issuing receipts before funds are cleared

A receipt should only be issued after the organization has actually received the funds. Issuing receipts prematurely, especially for cheques or pending transfers, may create discrepancies between financial statements and receipt records.

6. Poor reconciliation between receipts and bank deposits

Donation receipts must match accounting records and bank statements. Failure to reconcile regularly can result in unnoticed errors, duplicated entries, or missing funds. Consistent reconciliation strengthens financial control and audit readiness.

Manual receipt systems increase the risk of duplication and record inconsistencies. Regular internal checks can reduce these risks.

Digital Receipts and Compliance Modernization

Digital donation receipts are acceptable in Sri Lanka provided they include all mandatory elements and are securely stored. Many charities are transitioning to digital systems to enhance compliance and operational efficiency.

Digital systems help ensure:

- Automatic sequential numbering: This prevents duplicate or missing receipt numbers and maintains a clean audit trail.

- Reduced human error: Automation minimizes manual entry mistakes in amounts, donor names, and dates.

- Secure storage and backup: Digital records are easier to store safely and retrieve during audits.

- Faster donor acknowledgment: Receipts can be issued instantly, improving donor experience and transparency.

- Simplified audit preparation: Organized digital data allows quicker reconciliation and reporting.

Digital tools also improve tracking, reporting accuracy, and long-term compliance management. As regulatory expectations increase, adopting reliable digital solutions strengthens governance and financial transparency.

Strengthening Compliance with DonorKit

Managing donation receipts manually can expose charities to unnecessary compliance risks, particularly as transaction volumes grow. Ensuring accuracy in numbering, donor details, tax statements, and record retention requires consistent administrative control.

DonorKit is a specialized donation receipt software designed to support Sri Lankan registered charities in generating IRD-compliant donation receipts automatically. The system includes all mandatory fields, maintains proper sequencing, stores secure digital records, and reduces manual entry errors. By standardizing the receipting process, organizations can improve audit readiness and maintain regulatory compliance more efficiently.

For charities of all sizes, structured systems such as DonorKit support accuracy, accountability, and long-term compliance stability.

Conclusion

IRD-compliant donation receipt requirements in Sri Lanka are clear but strict. Registered charities must ensure that every receipt includes complete organizational details, donor information, accurate donation data, and proper authorization.

Compliance requires more than issuing receipts. It involves structured record-keeping, financial reconciliation, internal controls, and consistent adherence to Inland Revenue regulations.

Organizations that maintain accurate, transparent, and compliant receipting systems protect their tax status, safeguard donor trust, and strengthen their institutional credibility.

Maintaining compliance is not simply a regulatory requirement—it is a core element of responsible nonprofit governance in Sri Lanka.