For associations and nonprofits in France, issuing donation receipts is not just an administrative formality. It is a legal responsibility. A properly issued tax receipt allows donors to claim income tax reductions under French law. However, if a receipt does not meet official standards, the organization may face financial penalties and legal scrutiny.

Understanding the Donation Receipt Requirements France is therefore essential for every association authorized to issue tax receipts. These rules are governed by the French tax authority, the Direction Générale des Finances Publiques (DGFiP), which oversees compliance and enforces tax regulations.

This guide explains all the major rules, conditions, formatting requirements, eligibility criteria, risks, and practical examples of a compliant receipt in France. Whether you manage a small local association or a large national nonprofit, this article will help you stay compliant and confident.

Understanding the Legal Framework for Donation Receipts in France

In France, the right to issue tax-deductible donation receipts is based primarily on:

- Article 200 of the French General Tax Code (Code Général des Impôts) – for individuals

- Article 238 bis of the same Code – for corporate donors

Under these provisions, donors can benefit from a tax reduction if their contribution is made to an eligible organization and if they receive a valid tax receipt.

The DGFiP provides official guidance on what must be included in a receipt and which organizations are allowed to issue them. The official receipt format often referred to is “Cerfa Form n°11580*04”, which serves as the model tax receipt template.

Issuing a receipt without meeting eligibility requirements can expose an association to serious financial consequences, including penalties equal to 25% of the amounts wrongly stated on the receipt.

Which Organizations Are Allowed to Issue Tax-Deductible Receipts?

Before discussing formatting requirements, it is critical to understand eligibility.

Not every association in France can legally issue tax receipts.

An organization must meet the following conditions:

1. Nonprofit Character

The association must operate on a nonprofit basis. This means:

- No profit distribution to members

- Disinterested management

- Activities not primarily commercial

If the association competes directly with commercial businesses without offering significant public interest benefits, it may not qualify.

2. Public Interest Purpose (Intérêt Général)

The organization must pursue a public interest mission, such as:

- Humanitarian or social aid

- Education

- Scientific research

- Cultural promotion

- Environmental protection

- Sports development

- Religious activities (under specific conditions)

3. Proper Governance

Management must be disinterested. Board members cannot receive disproportionate compensation. Financial transparency must be maintained.

If there is any doubt about eligibility, associations can request a formal tax ruling (rescrit fiscal) from the DGFiP to confirm their right to issue receipts.

What Types of Donations Qualify?

Under French law, the following types of donations may qualify:

- Monetary donations (cash, bank transfer, cheque, online payment)

- Donations in kind (goods, equipment, materials)

- Abandonment of expenses by volunteers

- Corporate sponsorship (subject to rules under Article 238 bis)

However, donations must be made without any direct benefit in return. If the donor receives goods or services in exchange beyond symbolic recognition, the donation may lose its tax-deductible character.

Mandatory Information Required on a DGFiP Compliant Donation Receipt

A DGFiP compliant donation receipt must include specific elements. Omitting any of them may invalidate the document.

Here are the essential components:

1. Identification of the Organization

The receipt must clearly state:

- Full legal name of the association

- Registered address

- SIREN or RNA number (if applicable)

- Legal status (Association Loi 1901, Foundation, etc.)

2. Statement of Eligibility

The receipt must confirm that the organization meets the conditions under Articles 200 and/or 238 bis of the French General Tax Code.

3. Donor Information

The following details must be included:

- Full name of the donor

- Address of the donor

For corporate donors, company name and registered office address must be stated.

4. Date of Donation

The exact date when the donation was received must be mentioned.

5. Amount of Donation

The total amount received must be clearly stated in euros.

If the donation is in kind, a precise description and fair market value must be provided.

6. Nature of Donation

Specify whether the donation is:

- Monetary

- In-kind

- Abandonment of expenses

7. Receipt Number

Each receipt must have a unique sequential number for traceability.

8. Signature

The receipt must be signed by an authorized representative of the association.

Tax Reduction Rates for Donors in France

Understanding the donor benefit helps associations explain the value of compliance.

For Individuals (Article 200 CGI)

- 66% tax reduction of the donated amount: This means that if a donor contributes €100, they can reduce their income tax by €66, provided the organization qualifies under public interest criteria.

- Up to 20% of taxable income: The total amount of donations eligible for reduction cannot exceed 20% of the donor’s taxable income in a given year. Any excess can usually be carried forward.

For organizations assisting people in difficulty:

- 75% tax reduction (up to a certain threshold): Donations to organizations providing food, housing, or essential support to vulnerable individuals may qualify for a higher 75% reduction, subject to annual legal limits.

For Companies (Article 238 bis CGI)

- 60% tax reduction: Corporate donors can benefit from a tax reduction equal to 60% of the donated amount, making philanthropic partnerships financially attractive for businesses.

- Limited to 0.5% of annual turnover: The tax benefit for companies is capped at 0.5% of annual turnover. If the donation exceeds this threshold, the unused portion may generally be carried forward.

The receipt must correspond accurately to the donation amount and applicable legal article to ensure compliance and prevent disputes during a tax audit.

Specific Formatting Guidelines for a DGFiP Compliant Donation Receipt

Although associations in France are not strictly required to use the official Cerfa form template word-for-word, the structure and legal references must align with DGFiP standards. Any deviation that removes mandatory elements can invalidate the receipt.

Below are the essential formatting principles every association must follow.

Clear and Legible Layout

A donation receipt must be easy to read, professionally structured, and free from ambiguity. All mandatory information should be clearly separated and identifiable, including donor details, donation amount, legal references, and certification statements.

Using overly complex formatting, unclear fonts, or missing sections may create confusion during a tax audit. The DGFiP expects receipts to present information in a transparent and organized manner.

No Misleading or Promotional Language

A tax receipt is a legal document, not a marketing tool. It must not contain exaggerated claims, promotional statements, or misleading descriptions about tax benefits.

For example, the receipt should not suggest guaranteed tax refunds or imply benefits beyond what Articles 200 or 238 bis of the French General Tax Code legally allow. The wording must remain factual and compliant.

No Alteration of Legal Tax References

The references to Article 200 (for individuals) and Article 238 bis (for companies) must be accurate and unmodified. Associations must clearly indicate under which legal article the donation qualifies.

Altering or paraphrasing the legal text in a way that changes its meaning may be considered non-compliant. The legal basis for tax reduction must be stated precisely to ensure validity.

Proper Identification of the Applicable Article (200 or 238 bis CGI)

The receipt must clearly specify whether it applies to:

- Individual donors (Article 200 CGI), or

- Corporate donors (Article 238 bis CGI)

Using the wrong article reference may invalidate the donor’s tax claim. Associations that receive both individual and corporate donations should ensure their templates accommodate both scenarios correctly.

Unique and Sequential Receipt Numbering

Each donation receipt must have a unique number. Duplicate numbers or missing numbering sequences can raise serious concerns during a tax inspection.

Sequential numbering ensures traceability and allows authorities to reconcile issued receipts with recorded donations and accounting entries. Proper numbering also protects the association from accusations of misuse.

Digital Receipts and Integrity Standards

Digital or electronic donation receipts are permitted under French regulations, provided they maintain:

- Data integrity

- Secure storage

- Traceability

- Reproducibility during audits

Electronic receipts must contain all mandatory legal elements, just like paper receipts. Associations must be able to present them upon request from tax authorities.

Because maintaining consistency manually can be complex, many organizations now rely on structured systems such as Donation receipt software France solutions. These tools help ensure compliance, reduce formatting errors, and maintain accurate legal references aligned with DGFiP standards.

Recordkeeping and Audit Obligations

Issuing receipts is only part of compliance. Associations must also:

- Maintain donation records

- Keep copies of issued receipts

- Reconcile receipts with bank records

- Retain documentation for at least six years

If audited, the association must prove:

- The donation was actually received

- The donor did not receive improper compensation

- The organization was eligible to issue the receipt

Poor recordkeeping can create serious risk exposure.

Risks of Non-Compliance

Failure to respect Donation Receipt Requirements France can lead to:

- Financial penalties (25% fine on amounts improperly certified)

- Donor disputes

- Loss of credibility

- Revocation of tax receipt authorization

The DGFiP takes receipt misuse seriously, especially when public funds and tax reductions are involved.

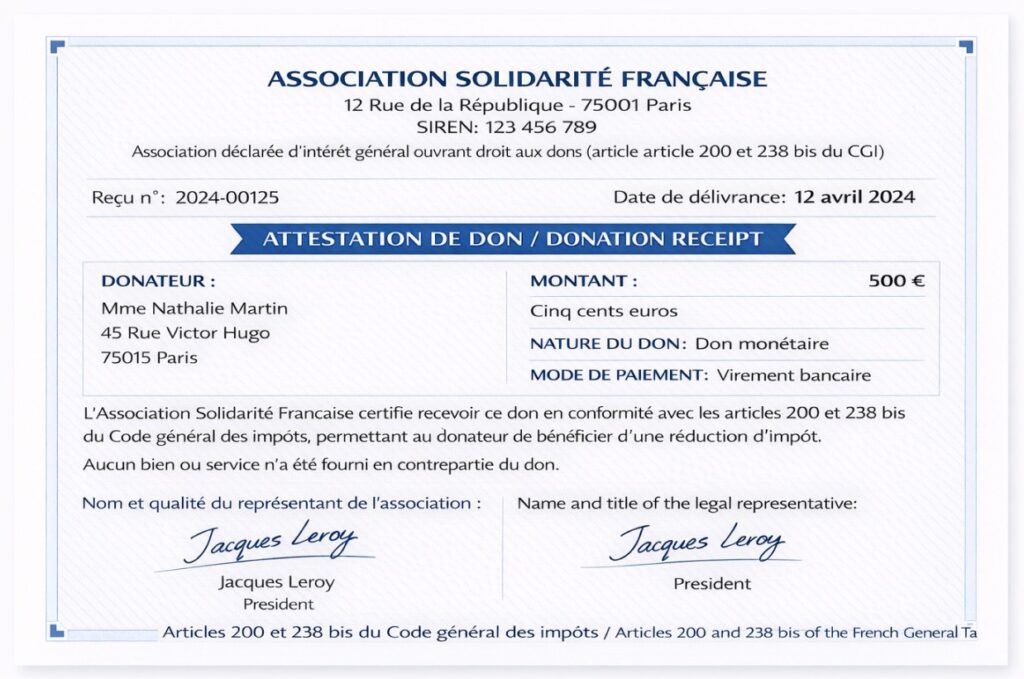

Example of a DGFiP Compliant Donation Receipt

Below is a simplified example of a compliant structure:

Association Solidarité France

123 Rue de la République

75000 Paris

SIREN: 123 456 789

Receipt No: 2025-00125

This receipt certifies that:

Mr. Jean Dupont

45 Avenue Victor Hugo

75016 Paris

Has made a donation of:

€500 (Five hundred euros)

Date of donation: 15 March 2025

Nature of donation: Monetary donation

The association certifies that it meets the conditions set out in Articles 200 and 238 bis of the French General Tax Code.

Issued in Paris, 16 March 2025

Signature

President of the Association

This format contains all mandatory legal elements required for compliance.

Sample DGFiP Compliant Donation Receipt Image for Reference

(This is a dummy receipt shown for illustration purposes only. All names and details are fictitious.)

Digital Receipts and Modern Compliance

French regulations allow electronic receipts, provided they:

- Contain all mandatory elements

- Ensure document integrity

- Are securely stored

- Can be reproduced during audits

As digital donations increase, many associations are turning to French charity donation receipt software to automate receipt issuance and prevent manual errors.

Using structured systems reduces:

- Numbering mistakes

- Missing tax references

- Inconsistent donor information

- Administrative burden

This is where specialized Nonprofit tax receipt software France becomes valuable.

How DonorKite Helps Associations Stay DGFiP Compliant

Managing receipts manually through spreadsheets or word processors increases the risk of human error. Incorrect numbering, missing legal references, or formatting inconsistencies can expose an association to penalties.

DonorKite is a professional donation receipt software designed specifically for compliance-driven nonprofits. It functions as a structured donation receipt generator software that allows associations to create accurate tax receipts aligned with French regulatory standards.

With DonorKite, organizations can:

- Automatically generate DGFiP-compliant receipts: Ensures every receipt includes mandatory French tax details, correct legal references, and structured formatting to meet official compliance standards.

- Maintain sequential numbering: Automatically assigns unique, traceable receipt numbers to prevent duplication errors and maintain proper audit documentation records.

- Store donor records securely: Keeps donor information organized and protected, making it easy to retrieve accurate data during tax reviews or inspections.

- Customize receipt templates to meet French requirements: Allows associations to align receipts with French legal rules while ensuring mandatory tax wording remains correct and intact.

- Issue digital receipts with full traceability: Generates secure electronic receipts that can be stored, tracked, and reproduced if requested by tax authorities.

- Reduce administrative workload through automation: Minimizes manual data entry, lowers human error risk, and saves staff time while maintaining structured compliance processes.

As a modern donation receipt generator, it simplifies complex compliance processes while reducing administrative workload.

Associations looking for an online donation receipt generator benefit from cloud-based access and secure document storage. This allows teams to manage donations efficiently while maintaining audit readiness.

By implementing structured systems that produce automated donation receipts for nonprofits, organizations significantly reduce compliance risks.

For associations seeking reliable Donation receipt software in France, DonorKite offers a practical solution that supports regulatory accuracy without operational complexity.

Conclusion

Complying with Donation Receipt Requirements in France is not simply a procedural task; it is a legal obligation that directly impacts donor trust and organizational credibility. Associations must ensure that every receipt contains accurate legal references, complete donor details, proper numbering, and clear certification under Articles 200 or 238 bis of the French General Tax Code. Even minor errors can create significant financial and regulatory risks. By maintaining structured documentation practices and adopting reliable systems that support accuracy and traceability, French associations can confidently issue DGFiP-compliant donation receipts while safeguarding both their donors and their mission.

Beyond regulatory compliance, properly structured donation receipts demonstrate transparency and professionalism. Donors who receive accurate and legally valid documentation are more likely to maintain long-term relationships with the organization. Clear and compliant receipts also reduce administrative back-and-forth during tax filing periods, strengthening donor confidence and operational efficiency.

As oversight and financial accountability expectations continue to increase in France, associations must treat donation receipt management as a core governance responsibility rather than a secondary administrative task. Establishing clear internal procedures, maintaining secure records, and using structured tools where necessary ensures that compliance remains consistent, sustainable, and aligned with DGFiP standards.